This is the editorial commentary to accompany the cap hpi guide to future residual values for new cars.

The content is as follows:

- gold book forecast accuracy

- Forecast changes this month

- Market overview

- gold book methodology

- Reforecast calendar 2017/2018

1. gold book Forecast Accuracy

As gold book matures since its introduction in December 2013, we have the data to enable us to measure our results in terms of forecast accuracy. The accuracy target widely demanded by our customers is to be within 5% of actual values and we are pleased that, averaged across all models, gold book has been within this target since launch.

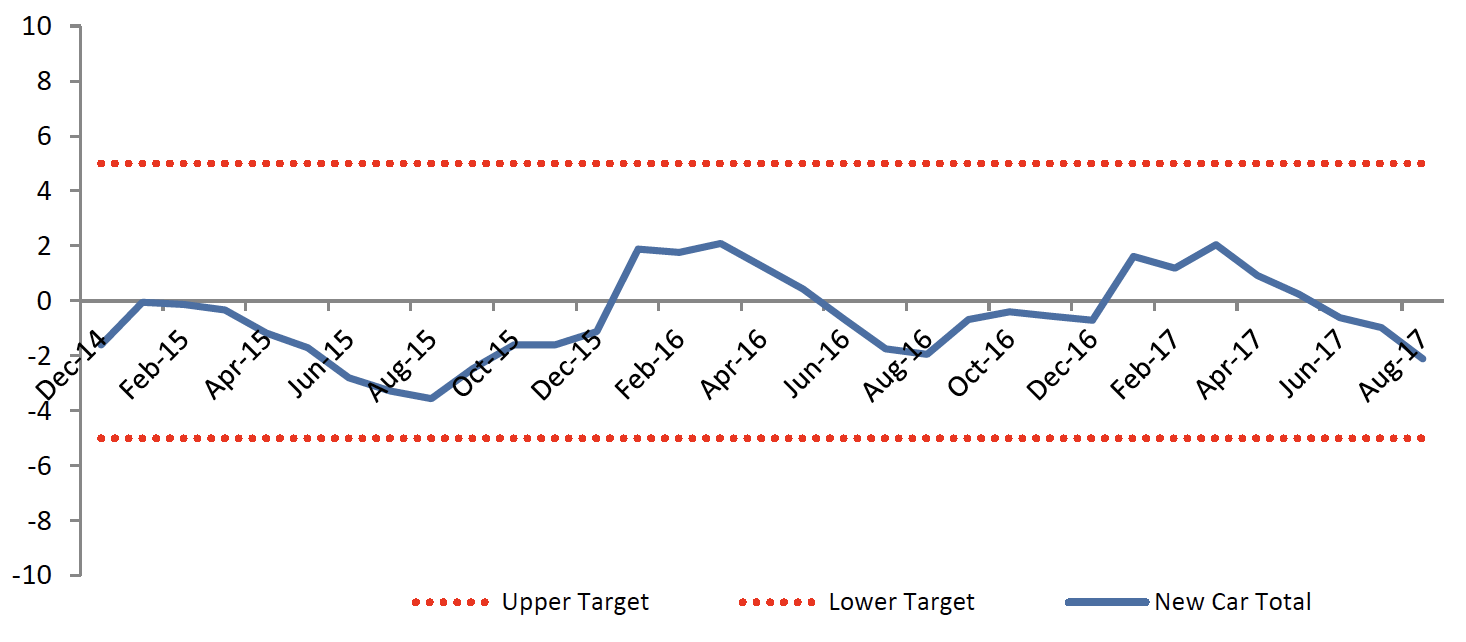

12 month results

Since measurement started our 12 month forecasts have averaged -0.6% less than black book across all vehicle ids, and the most recent results show August 2016 12/20 gold book forecasts being -2.1% less than August 2017 12/20 black book.

The latest 12/20 forecast differences for the major vehicle sectors are outlined below:

|

Sector |

Ave GB Diff% |

|

City Car |

4.1% |

|

Executive |

-3.2% |

|

Lower Medium |

1.1% |

|

MPV |

-4.5% |

|

Supermini |

-3.7% |

|

SUV |

-6.6% |

|

Upper Medium |

1.3% |

|

Grand Total |

-2.1 |

We remain within our general customer target of +/-5% across most of the major sectors. SUV has now just fallen outside of target but we expect the reforecast changes we made in October 2017 will bring it back within target soon.

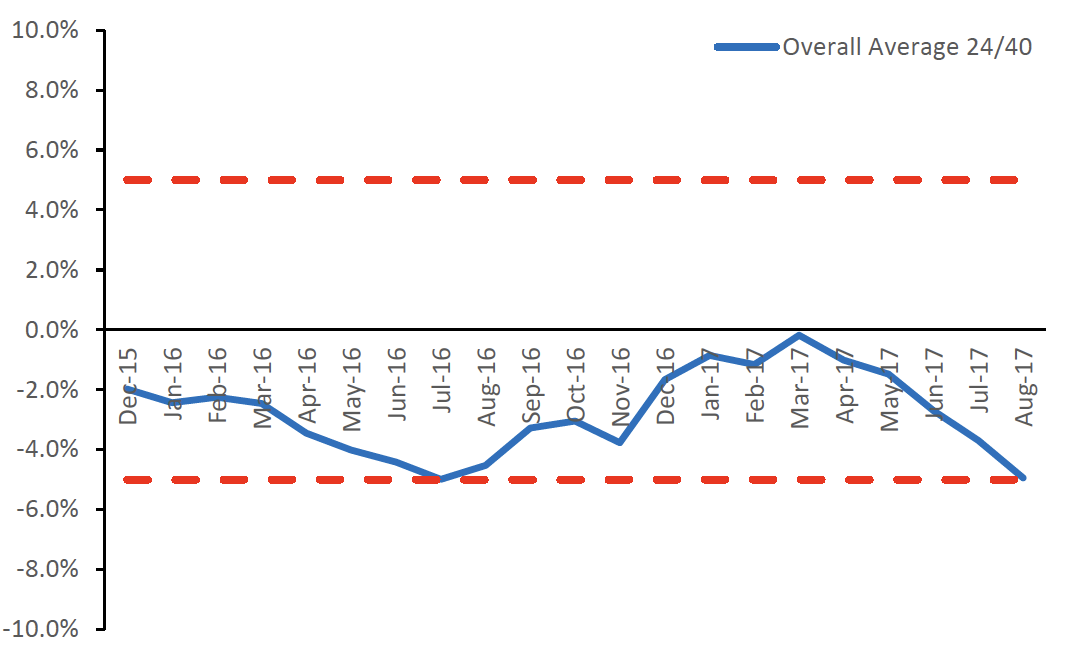

24 month results

Since measurement started our 24 month forecasts have averaged -2.8% less than black book across all vehicle ids, and the most recent results show August 2015 24/40 gold book forecasts being -4.9% less than August 2017 24/40 black book.

The latest 24/40 forecast differences for the major vehicle sectors are outlined below:

|

Sector |

GB Diff % |

|

City Car |

6.2% |

|

Executive |

-2.9% |

|

Lower Medium |

-3.6% |

|

MPV |

-8.1% |

|

Supermini |

-3.8% |

|

SUV |

-9.4% |

|

Upper Medium |

-3.8% |

|

Grand Total |

-4.9 |

We are within or very close to our general customer target of +/-5% across the majority of the major sectors. Exceptions are City Car where the average difference between current black book and our previous forecast is more significantly above the upper limit, due to the unexpectedly high level of forced registration activity in this sector throughout 2015 and 2016 which forced values down, so we took corrective action in our sector reforecasts and this will improve future accuracy; and MPV and SUV where again we took corrective action in our sector reforecasts and this will improve future accuracy.

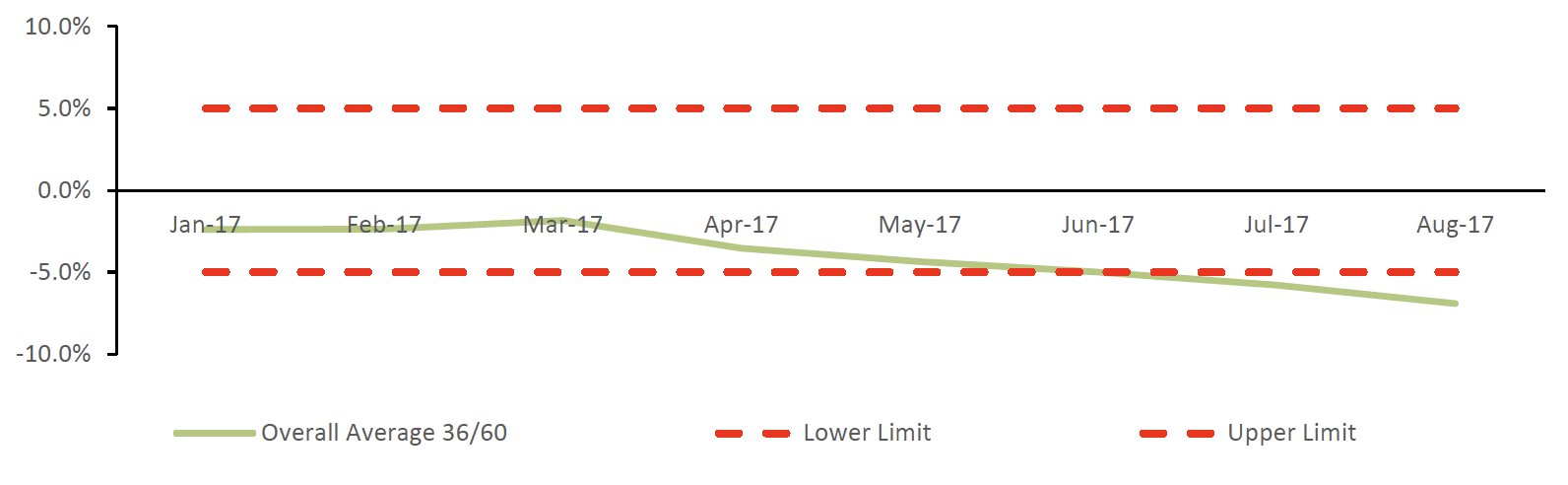

36 month results

Since measurement started our 36 month forecasts have averaged -4.0% less than black book across all vehicle ids, and the most recent results show August 2014 36/60 gold book forecasts being -6.9% less than August 2017 36/60 black book. Although these is slightly outside target these are the results from very early gold book forecasts and we are analysing historic sector reviews to determine likely future performance.

Overall results

Although this remains the early stages, we continue to be extremely pleased with these initial results. We are taking advantage of our new methodology to implement a ‘virtuous feedback loop’, with each element of the forecast examined to determine how best to further improve the accuracy of our future value forecasts, while also reducing variation.

Our used market deflation (YOY%) assumptions, differentiated by age, vehicle sector and fuel type are still broadly in line with the current market at the vast majority of points.

We will continue to publish these results and share them with our customers.

2. Forecast changes this month:

New model ranges added this month:

Citroen C3 Aircross, Maserati GranTurismo, Maserati GranCabrio, Maserati Levante, Mercedes-Benz S Class, Mitsubishi Eclipse and Ssangyong Rexton.

There are numerous additions to the following model ranges:

BMW 1 Series, BMW X1, Ford Focus, Ford Ka+, Ford Mondeo, Kia Niro, Maserati Quattroporte, Mercedes-Benz G Class, Mercedes-Benz GLC, Mercedes-Benz GLC Coupe, Nissan Micra, Nissan Pulsar, Nissan X-Trail, Seat Ibiza, Skoda Octavia, Toyota Rav4 and Vauxhall Insignia Country Tourer.

Sectors reforecast this month

This month, we publish our most recent reforecasts for the Upper Medium, Executive, Large Executive, and Luxury Executive sectors.

The overall impact of the changes at 36/60 is set out below:

|

Sector |

Underlying Forecast Change |

Seasonal Element |

Observed Change Aug vs Jul |

|

Upper Medium Petrol Upper Medium Diesel Executive Petrol Executive Diesel Large Executive Petrol Large Executive Diesel Luxury Executive Petrol |

+2.5% -0.7% +2.3% +1.2% -0.1% -3.8% +1.5% |

+3.2% +3.5% +2.8% +3.1% +2.8% +3.5% +3.1% |

+5.7% +2.8% +5.1% +4.3% +2.7% -0.3% +4.6% |

The observed (published) changes are almost entirely positive, assisted by positive impact of September seasonality due to the new registration plate.

However the underlying forecast changes are also relatively positive, reflecting market strength in these sectors, and the fact we have not changed any future market deflation assumptions for these sectors. In particular, we consider that diesel engines, where available, will still continue to be attractive in these larger cars and that our current diesel deflation assumptions are suitable to carry forward.

Note that Large Executive Diesel Sector only has a very small number of models, and the average movement is skewed by the movement on BMW 7 series.

Other forecast changes this month

Aside from the sector reforecasts, there have been other changes this month to the following ranges:

Changes to walk up (subsidiary) relationships following analysis of the most recent black book research:

-

Aston Martin Vanquish: increased walk up to S trim, following further specification information received from the manufacturer.

-

Toyota RAV4: decreased walk-up for satnav, to align with latest black book research.

Seasonality changes

In line with our gold book methodology, all other model ranges which are outside of the sector reforecasts and outside of the other changes listed above, have had their values moved forward from month to month by seasonal factors which are differentiated by sector and fuel type and are based on analysis of historical black book movements.

Overall impact on forecasts

The overall average change between the new gold book forecast and the previous gold book forecast is approximately +3.5% at 36/60, which is in line with normal expectations of the seasonal change for full year forecasts between August to September.

Details of all values revised by ±5% can be found via the following link: Monthly Reports

3. Market Overview

Following the vote to leave the EU, Article 50 has been invoked, but it remains clear that this is just the beginning of a complicated process which will take at least 2 years to conclude with us actually ceasing to be an EU member, probably considerably longer. The outcome will not start to become clear until negotiations are well underway but future trade agreements which negatively impact the UK economy (and that of other major EU states) are still considered unlikely. The result of the recent general election in the UK appears likely to favour a soft rather than hard Brexit.

HM Treasury published new forecasts in June, which are little changed from the previous February forecasts. These were slightly more positive that the previous November forecasts, which were themselves slightly more positive than the previous August forecasts. Therefore, the latest forecasts remain in line with our own view, with a slight reduction in GDP in 2017 and 2018 but recovering thereafter. Not all ages and sectors of vehicle are directly impacted by GDP, and in some cases this will be offset by lower future registration volumes. Forecasts for inflation and unemployment show no signs for concern.

We expect some mildly negative effects on the economy in the short to medium term, due to reduced business capital expenditure and investment, but expect consumer spending to continue to drive a stable economy. The protracted nature of the Brexit will allow time to assess the most likely outcome and future forecast published by HM Treasury, therefore at present we are planning to conform to our original timetable of sector reforecasts and do not consider it necessary to embark on wholesale reforecasts.

As leasing and PCP returns increase and more nearly new cars return to the used marketplace, values are broadly expected to decrease in line with previous seasonal aging patterns, with negative impact from a slowing economy mitigated by the effects of decreased supply.

In the coming months, used car supply is expected to increase further, however in general we do not expect to see significant decreases in three or four-year-old values in the next 12 months over and above typical model aging patterns, with supply and demand remaining broadly in balance. Our forecasts incorporate the effect of increased registrations on individual sectors, with variation in the level of impact and which part of the market the sectors are sensitive to.

In 2017, despite an expected buoyant Q1 boosted by the VED changes, we expect new car registration volumes to fall. The movement in Exchange rates since the Brexit referendum is likely to make the UK less attractive for forced registrations in 2017, and registration volumes are increasing in a number of European countries, where the pent up demand for new cars may help divert some volume from the UK. Fairly high forced registration volumes continued in the early part of the year, with a pull from April into March due to VED changes, but we expect a tailing off later in the year.

The trend in recent years for new car registrations has been a slow move away from diesel into petrol and alternative fuels, and for used diesel values to deflate slightly more than petrol values. However this varies by vehicle sector, and is most marked in small car sectors whereas in larger car sectors where diesel makes most sense, there has been little or no impact. We expect these trends to continue in future years, with some acceleration of diesel deflation in the smaller car sectors.

Demand Outlook

The outlook for the UK economy is uncertain in the context of Brexit but the consensus of the latest independent forecasts for GDP is no cause for alarm. Making decisions on interest rate changes based on % unemployment is far less reliable than it has been in the past and we are continuing to investigate whether we can usefully integrate any additional labour market metrics into our regression modelling (currently % unemployment is one of 15 labour market metrics studied). The unemployment rate remains low at 4.4%, and wage growth remains relatively slow by historic standards, especially given current labour market conditions.

On 4th August 2016 the Bank of England base rate was cut from 0.5% to 0.25%, and interest rates are expected to remain low for the medium term. Any significant increases in base rates still seem unlikely until there is a combination of further improvements in wage growth and increases in rates of headline inflation.

CPI continues to creep up due to the sterling exchange rate and is now at +2.6%, which is almost a 2-year high and exceeds the Bank of England’s lower limit of +2%. RPI is at 3.6%. Oil prices remain very hard to predict, with the situation changing on an almost daily basis. As predicted, the glut of production from leading OPEC countries proved to be unsustainable and it remains to be seen whether this action will be enough to force small producers out of the market. During October, the OPEC countries agreed to an initial cut production, which has now been extended for a further 9 months which should help to ensure market stability. When supply returns to levels commensurate with demand, oil prices are likely to rise steadily over the forecast period, but fuel prices will remain well below historic levels unless there are significant currency movements against the US Dollar. Wage growth remains reasonably healthy, although slow by historical standards, although if earnings continue to outstrip price inflation as expected, then that will continue to provide a positive impetus to the overall economy.

GDP growth for the UK was stronger than expected in Q416 (+0.6%) giving annualised growth of +2% over 2016 (compared to +2.2% over 2015). GDP fell back to 0.3% in Q1 2017 and remains at this level in the recently published figure for Q2 2017. The most recent June publication of independent forecasts by HM Treasury (predicting a small drop in GDP in 2017 and 2018 followed by recovery) have been studied in great detail and it seems that the biggest reductions in forecasts have come from those who were originally much more bullish about the UK economy’s prospects than the central projection. In conclusion, even a marginal recession seems unlikely.

Consumer and Business Confidence had continued to slowly increase as we had expected, although post the Brexit referendum we now expect to see a decline in overall business investment, reversing the recent trend, particularly in the large corporate sector. Much of the previous export growth was driven by the service sector, but this has slowed in recent months and there have also been increases in manufacturing and domestic car output. Much of this activity reflected the shift in export focus from the Eurozone to emerging economies and this is likely to continue, despite fluctuating Eurozone demand (see below), although exports still remain below the long term average. The UK will remain within the European Economic Area for the foreseeable future and despite recent statements from the EU and the UK government, it is difficult to envisage a realistic scenario whereby motor vehicles would not be part of a tariff free arrangement in the future.

Forecasts for future house price increases vary dramatically by sector and especially by geography. Despite a view expressed by the Bank of England’s Financial Stability Committee that the buy to let sector could “amplify” any boom or bust in the housing market, any negative effects are likely to be centred on London, with the rest of the country significantly more insulated from the impact of any such downturn. The ‘new powers’ being proposed are unlikely to have any significant impact as the buy to let market is expected to reduce following previous tax measures announced by the government.

Supply Outlook

New car registrations for 2016 came in at 2.69 million, with short cycle volumes and forced registrations a significant factor for several manufacturers in the final weeks of the year. We originally expected the 2016 total to be slightly lower than 2015, with growth faltering from the second quarter onwards. However, forced registrations continued so that the year ended ahead of 2015.

Exchange rates are a major influence on the profitability of the UK new car market and they strongly influence eventual used vehicle volumes. Sterling rates against the Euro reduced as expected from around 1.43 in November 2015, to averaging 1.26 in April 2016 – equivalent to a -12% decrease in Euro revenue for the same vehicle sale - then fell further and have averaged 1.14 over the last 3 months. An increase in rates before the EU referendum exaggerated the falls following the vote, but rates remain slightly below our expectation. We had expected further modest short term reductions before a more gradual decrease in the Sterling rate against the Euro over the next 3 years, as growth continues to pick up in mainland Europe.

The shift in exchange rates will make the UK less profitable for manufacturers and the SMMT have forecast reduced registrations for 2017 at around 2.55M. We believe the figure could be lower depending on the impact on forced registrations, despite an expected buoyant Q1 2017 which was 6.2% up on Q1 2016 due to the effect of VED changes due in April. If any manufacturers continue to pursue market share at the expense of profitability, then the impact on used values will continue to worsen, and we will continue to apply a number of specific model adjustments in gold book which have been outlined in gold book iQ.

The UK economic situation looks likely to continue to offset any remaining weakness in the Eurozone and Sterling is set to remain at a level which should limit manufacturers’ scope for heavy discounting through 2017.

New car registrations in other key European market continue to grow as a result of the release of pent up demand. In the three years before the financial crisis, France, Germany, Italy and Spain represented an annual combined volume of almost 9.4 million units, and have recovered to 7.7 million in 2015 and then 8.3M in 2016, suggesting there is further growth to come. Spanish growth may well slow in 2017 following the removal of scrappage incentives, but the other key markets appear to be growing steadily and vehicle lead times are expected to increase.

4. Gold Book Methodology:

Overview

All of our future residual values are based on the gold book methodology. Our values take current month black book values as a starting point (uplifted for model changes where necessary), are moved forward according to age/sector/fuel specific year on year deflation assumptions regarding future used car price movements, and are then subjected to additional adjustments by the Editorial Team. Finally the values are moved forward by the next month’s seasonality adjustments which are differentiated by sector and fuel type and are based on analysis of historical black book movements.

All of these assumptions and adjustments are available for scrutiny to our customers through our gold book iQ product. For years our customers have been asking for transparency in automotive forecasting and we have delivered a ground-breaking product to provide exactly that.

With an increasing number of customers subscribing to gold book iQ, we are entering into a range of debates and discussions around both our overall forecasting methodology and individual elements of the forecasts for particular vehicles. This is expected to evolve over time into a ‘virtuous circle’, with the feedback looping back into the forecast process and delivering continuous improvement. We are embracing a new era of customer communication, with a greatly improved quality of interaction and debate around our forecast values.

Changes may be actioned wherever there is reason to do so outside of the sector reforecast process and we continue our monthly Interproduct analysis with our black book colleagues exactly as before. This has intensified following the availability of our short term forecast data (gold book 0-12, now available to customers), which incorporates detailed exception reporting at a cap hpi ID level and will also be used increasingly going forward to manage the relationships between black book and gold book.

Forecasting Model Development - gold book & iQ

gold book iQ was launched in December 2013 and gives unparalleled transparent insight into the assumptions used to produce our forecasts. The feedback from customers to date has been extremely positive and we believe gold book iQ will represent a new benchmark in truly market leading forecasting. More details are available here: http://business.cap.co.uk/products-and-services/gold-book-iQ

Our short term forecast product, gold book 0-12, (also marketed as black book +12) has now been launched and is available to customers. This is a live, researched product with a dedicated Editor (Rob Hester) and fills a gap in our previous forecast coverage. See link to a previous podcast http://www.cap.co.uk/en/cap-extras/its-the-saturday-morning-meeting-on-motor-trade-radio/

Following feedback on our gold book iQ product, from September 2016 we have added more detail into the commentary for each model range reforecast in sector reviews. We will continue to review and enhance commentary in future months as we carry out each sector review.

Forecast Output

Individual forecasts are provided in pounds and percentage of list price for periods of twelve to sixty months with mileage calculations up to 200,000.

Each forecast is shown in grid format with specific time and mileage bands highlighted for ease of use.

All forecast values include VAT and relate to a cap hpi clean condition and in a desirable colour.

All new car prices in gold book include VAT and delivery.

Parallel Imports

Particular care must be taken when valuing parallel imports. Vehicles are often described as full UK specification when the reality is somewhat different. These vehicles should be inspected to ensure that the vehicle specification is correct for the UK. Parallel imports that are full UK specification and first registered in the UK can be valued the same as a UK-sourced vehicle.

Grey Imports

cap hpi gold book does not include valuations for any grey import vehicles, (i.e. those not available on an official UK price list).

5. Reforecast Calendar 2017/2018:

Monthly Product

Sector 1

Sector 2

Sector 3

Sector 4

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

Apr-18

May-18

Jun-18

Jul-18

Aug-18

Sep 18

MPV

Lower Medium

City Car

SUV

Upper Medium

MPV

Lower Medium

City Car

SUV

Upper Medium

MPV

Lower Medium

Convertible

Sports

Supermini

Electric

Executive

Convertible

Sports

Supermini

Electric

Executive

Convertible

Sports

Coupe Cabriolet

Supercar

Large Executive

Coupe Cabriolet

Supercar

Large Executive

Coupe Cabriolet

Supercar

Luxury Executive

Luxury Executive