The New Year got off to a good start in the used LCV Wholesale Market judging from our observations at auctions and from the sales results we have seen so far. With plenty of used LCV stock around trade buyers were out in force and there was fierce competition between hall and internet buyers for the most desirable lots.

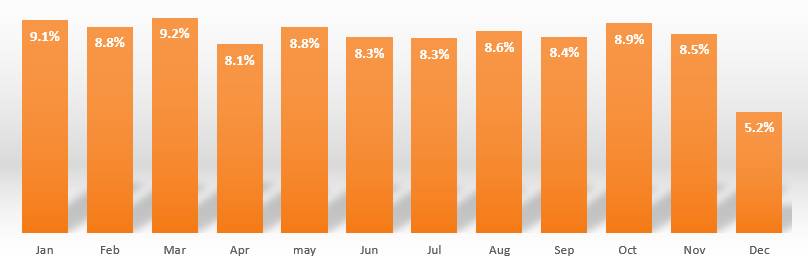

This surge in auction activity during January is seen most years as reflected in the historical sales records. The chart below shows the monthly sales volumes expressed as a percentage of the total number of annual sales. Over the past 5 years sales volumes have typically dropped by around 3.4% in December then bounce back to around 9.1% in January.

Monthly Sales Percentage of Annual Sales - 5 year trend

With fewer auction sales to attend and many buyers taking extended holiday breaks over the Christmas period the market tends to slow down in December. However, according to some vendors and auctions officials we have spoken to many of the larger used LCV retailers were noticeably cutting-back on spending around mid-November. Arguably this had more to do with the cloud of political and economic uncertainty that was hanging over the country than the forthcoming holidays.

It remains to be seen if January’s bustling auctions halls and healthy sales conversion rates represents a turning point in the market or if it’s simply a release of pent-up demand as we have seen in previous years.

Sales Performance Trend by Sector

|

November |

December |

January |

|

|

LCV Sector |

Performance |

Performance |

Performance |

|

City Van |

101.3% |

99.2% |

100.0% |

|

Small Van |

100.0% |

100.4% |

99.9% |

|

Medium Van |

101.0% |

101.2% |

101.9% |

|

Large Van |

100.8% |

100.3% |

99.9% |

|

Over 3.5T |

98.6% |

101.7% |

99.1% |

|

4x4 Pick-up Workhorse |

100.0% |

101.0% |

101.1% |

|

4x4 Pick-up Lifestyle SUV |

101.0% |

101.2% |

101.2% |

|

Forward Control Vehicle |

98.2% |

94.1% |

101.6% |

|

Chassis - Derived |

99.7% |

102.5% |

100.3% |

|

Minibus |

102.9% |

94.3% |

97.1% |

|

Vat Qualifying |

98.9% |

97.2% |

99.2% |

|

Total Market |

100.6% |

100.7% |

100.7% |

Market prices remained relatively stable last month with most sectors performing well against the guide values and only the Minibus sector significantly under-performing.

Please note that all references to sector market shares and price performances against the guide are in relation to the research data we collect and analyse each month in order to determine changes that may need to be made to the guide values.

Guide Price Adjustment in this Editon

The guide prices of most models across of the LCV sector have gone down on average by around 0.4% in this edition.

Using 3 years / 60,000 miles as a benchmark, the average percentage and monetary movements shown in the table below give an indication of the extent of the price adjustments that were necessary in order to reflect current market prices for this edition.

|

February: LCV Used Guide Price Movements 3 year / 60k |

||

|

LCV Sector |

Average % Movement |

Average £ Movement |

|

City Van |

-0.8% |

-£32 |

|

Small Van |

-0.8% |

-£39 |

|

Medium Van |

-0.5% |

-£49 |

|

Large Van |

-0.3% |

-£29 |

|

Over 3.5T |

-0.7% |

-£89 |

|

4x4 Pick-up Workhorse |

0.2% |

£14 |

|

4x4 Pick-up Lifestyle SUV |

-0.3% |

-£35 |

|

Forward Control Vehicle |

-1.0% |

-£119 |

|

Chassis - Derived |

-0.7% |

-£74 |

|

Minibus |

-1.0% |

-£139 |

|

Vat Qualifying |

-1.1% |

-£124 |

Top selling models in the used LCV Wholesale Market

The following tables contain the Top 10 selling models ranked in sales volume order. They aim to provide an overview of the models in each sector that were driving trade market prices across the used LCV Wholesale Market as a whole.

City Vans

|

CAPId |

City Van |

|

26326 |

FIESTA DIESEL - 1.6 TDCi ECOnetic Van |

|

26324 |

FIESTA DIESEL - 1.5 TDCi Van |

|

34481 |

FIESTA DIESEL - 1.5 TDCi Sport Van |

|

34479 |

FIESTA DIESEL - 1.5 TDCi ECOnetic Van |

|

30871 |

TRANSIT COURIER DIESEL - 1.5 TDCi Trend Van |

|

30873 |

TRANSIT COURIER DIESEL - 1.6 TDCi Trend Van |

|

34795 |

BIPPER DIESEL - 1.3 HDi 75 Professional [Nav] [non Start/Stop] |

|

15140 |

BIPPER DIESEL - 1.4 HDi 70 S |

|

24217 |

NEMO DIESEL - 1.3 HDi Enterprise [non Start/Stop] |

|

24228 |

BIPPER DIESEL - 1.3 HDi 75 S [non Start/Stop] |

With most models in the City Van sector achieving the guide prices last month, on average, only a marginal price adjustment of -0.8% was necessary in this edition. This amounts to around -£32 on a 3-year plate at 60K, however, there are some notable exceptions which are listed below.

Astravan continues to appear in the market in relatively high numbers despite it being discontinued by Vauxhall in 2012. Whilst the guide values of these models have gone down by 2%, with an average market price of around £1040, this amounts to a price drop of around £20.

|

Models |

|

|

VAUXHALL ASTRAVAN (06-13) VAN (-2%) |

PEUGEOT BIPPER (08-17) VAN (1%) |

|

VAUXHALL CORSAVAN (07-19) VAN (1%) |

VAUXHALL ASTRAVAN (98-06) PET VAN (-2%) |

|

CITROEN NEMO (08-16) VAN (-2%) |

VAUXHALL ASTRAVAN (98-06) VAN (-2%) |

|

FIAT FIORINO (08-16) VAN (-2%) |

Small Vans

|

CAPId |

Small Van |

|

38471 |

BERLINGO L1 DIESEL - 1.6 BlueHDi 625Kg Enterprise 75ps |

|

18445 |

BERLINGO L1 DIESEL - 1.6 HDi 625Kg Enterprise 75ps |

|

20709 |

CADDY MAXI C20 DIESEL - 1.6 TDI 102PS Van |

|

28276 |

CADDY MAXI C20 DIESEL - 1.6 TDI 102PS Startline Van |

|

18590 |

DOBLO CARGO MAXI LWB DIESEL - 1.6 Multijet 16V Van Start Stop |

|

28266 |

CADDY C20 DIESEL - 1.6 TDI 102PS Startline Van |

|

37702 |

TRANSIT CONNECT 200 L1 DIESEL - 1.5 TDCi 120ps Limited Van |

|

38515 |

PARTNER L1 DIESEL - 850 1.6 BlueHDi 100 Professional Van [non SS] |

|

24234 |

COMBO L1 DIESEL - 2000 1.3 CDTI 16V H1 Van |

|

34756 |

CADDY C20 DIESEL - 2.0 TDI BlueMotion Tech 102PS Startline Van |

Representing around 23% of all used LCV sales in our research data and with a sales performance of 99.9% against the guide, it was another strong month for the Small Van sector. On average the guide prices have gone down £39 or 0.8% with the following notable exceptions.

|

Models |

|

|

FORD CONNECT (18- ) T200-T240 VAN (3%) |

CITROEN BERLINGO (02-12) VAN (-6%) |

|

M-B CITAN (13-19) VAN (-2%) |

CITROEN BERLINGO (98-09) PET VAN (-6%) |

|

VW CADDY E6 (16- ) VAN (-2%) |

FORD CONNECT (02-07) T200 PET VAN (-3%) |

|

FORD CONNECT (13-19) T200-T240 VAN (1%) |

FORD CONNECT (02-08) T210 PET VAN (-3%) |

|

RENAULT KANGOO (13-17) VAN (0%) |

FORD CONNECT (02-09) T200-T230 VAN (-3%) |

|

VAUXHALL COMBO E6 (16-19) VAN (0%) |

FORD CONNECT (06-07) T210 VAN (-3%) |

|

VW CADDY (15-17) VAN (2%) |

PEUGEOT PARTNER (96-08) PET VAN (-6%) |

|

FIAT DOBLO CARGO (10-17) VAN (0%) |

PEUGEOT PARTNER (96-10) VAN (-6%) |

|

FORD CONNECT (09-13) T200-T230 VAN (1%) |

VAUXHALL COMBO (01-10) PET VAN (-2%) |

|

VAUXHALL COMBO (12-18) VAN (-2%) |

VAUXHALL COMBO (01-12) VAN (-2%) |

|

VW CADDY (10-15) C20 VAN (-2%) |

VW CADDY (04-10) C20 VAN (-3%) |

Medium Vans

CAPId

Medium Van

25441

TRANSIT CUSTOM 270 L1 DIESEL FWD - 2.2 TDCi 125ps Low Roof Limited Van

35797

TRANSIT CUSTOM 270 L1 DIESEL FWD - 2.0 TDCi 130ps Low Roof Limited Van

25437

TRANSIT CUSTOM 270 L1 DIESEL FWD - 2.2 TDCi 100ps Low Roof Van

25458

TRANSIT CUSTOM 310 L1 DIESEL FWD - 2.2 TDCi 125ps Low Roof Van

35807

TRANSIT CUSTOM 290 L1 DIESEL FWD - 2.0 TDCi 105ps Low Roof Van

31721

VIVARO L1 DIESEL - 2700 1.6CDTI BiTurbo 120PS ecoFLEX Sportive H1 Van

10564

PRIMASTAR 2.9T LWB DIESEL - 2.0 dCi SE Van 115ps

25475

TRANSIT CUSTOM 290 L2 DIESEL FWD - 2.2 TDCi 125ps Low Roof Limited Van

38112

VIVARO L2 DIESEL - 2900 1.6CDTI 120PS Sportive H1 Van

42077

TRANSIT CUSTOM 300 L2 DIESEL FWD - 2.0 EcoBlue 130ps Low Roof Limited Van

Accounting for just under 30% of all used LCV sales in our research data last month, Medium Van is by far the largest and most complex of all the LCV sectors. With so many vans sold in this sector each month it serves as a market sentiment indicator for the entire LCV wholesale market.

It’s encouraging to see that prices held firm in November and December at around 101% and we saw further strength in January at 101.9%. However, after considering the under-performance of certain models and over-performance of others, some changes were made to the guide prices in this sector. Whilst the overall impact of these is only around -0.5% or -£49 on a 3-year plate/60K, the following ranges have some significant price adjustments.

|

Models |

|

|

FORD TRANSIT CUSTOM VAN E6 (17- ) (1%) |

VAUXHALL VIVARO E6 (16-19) VAN (1%) |

|

M-B VITO E6 (15- ) CDi VAN (0%) |

VW T6 TRANSPORTER (15-16) VAN (3%) |

|

PEUGEOT EXPERT E6 (16- ) VAN (1%) |

M-B VITO (03-11) CDi FRIDGE (4%) |

|

RENAULT TRAFIC E6 (16-20) dCi VAN (3%) |

M-B VITO (03-11) CDi VAN (4%) |

|

M-B VITO (10-15) CDi VAN (2%) |

M-B VITO (03-11) DUALINER VAN (4%) |

|

M-B VITO (10-15) DUALINER VAN (4%) |

VAUXHALL VIVARO (14-18) VAN (1%) |

|

NISSAN PRIMASTAR (06-15) dCI VAN (4%) |

M-B VITO (05-07) PET VAN (4%) |

|

PEUGEOT EXPERT (07-16) VAN (1%) |

VAUXHALL VIVARO (11-14) VAN (-3%) |

|

RENAULT TRAFIC (14-16) dCi VAN (2%) |

VW T5 TRANSPORTER (03-10) VAN (-4%) |

Large Vans

CAPId

Large Van

38198

BOXER 335 L3 DIESEL - 2.0 BlueHDi H2 Professional Van 130ps

26863

SPRINTER 313CDI LONG DIESEL - 3.5t High Roof Van

31217

RELAY 35 L3 DIESEL - 2.2 HDi H2 Van 130ps Enterprise

30637

TRANSIT 350 L3 DIESEL RWD - 2.2 TDCi 125ps H3 Van

36890

SPRINTER 314CDI MEDIUM DIESEL - 3.5t High Roof Van

31888

MOVANO 35 L3 DIESEL FWD - 2.3 CDTi BiTurbo ecoFLEX H2 Van 136ps

36948

SPRINTER 314CDI LONG DIESEL - 3.5t High Roof Van

9104

TRANSIT 260 SWB DIESEL FWD - Low Roof Van TDCi 85ps

31707

BOXER 335 L3 DIESEL - 2.2 HDi H2 Professional Van 130ps

27306

SPRINTER 313CDI MEDIUM DIESEL - 3.5t High Roof Van

At 99.9% the price performance of the Large Van sector was marginally below the guide. Whilst the guide values have moved down on average by 0.3% or -£49, there are several notable exceptions where prices remain the same as last month.

|

Models |

|

|

FORD TRANSIT E6 (19- ) T290 - T350 VAN (3%) |

VW CRAFTER (06-17) VAN (0%) |

|

IVECO DAILY E6 (19- ) VAN (0%) |

IVECO DAILY (06-09) VAN (0%) |

|

FIAT DUCATO (14- ) VAN (0%) |

IVECO DAILY (06-10) 3.5t VAN (0%) |

|

FORD TRANSIT E6 (16-19) T290 - T350 VAN (3%) |

IVECO DAILY (99-07) L CLASS VAN (0%) |

|

IVECO DAILY E6 (14-19) VAN (0%) |

IVECO DAILY CNG (04-07) VAN (0%) |

|

IVECO DAILY (09-15) VAN (0%) |

IVECO UNIJET DAILY (03-06) L CLASS VAN (0%) |

|

IVECO DAILY (14-16) VAN (0%) |

IVECO UNIJET DAILY (03-07) C CLASS VAN (0%) |

|

RENAULT MASTER (10-17) dCi VAN (0%) |

IVECO UNIJET DAILY (03-07) S CLASS VAN (0%) |

4x4 Pick-ups Lifestyle

CAPId

4x4 Pick-up Lifestyle SUV

35006

RANGER DIESEL - Pick Up Double Cab Wildtrak 3.2 TDCi 200 Auto

35284

L200 DIESEL - Double Cab DI-D 178 Barbarian 4WD

35285

L200 DIESEL - Double Cab DI-D 178 Barbarian 4WD Auto

39511

NAVARA DIESEL - Double Cab Pick Up Tekna 2.3dCi 190 4WD Auto

39510

NAVARA DIESEL - Double Cab Pick Up Tekna 2.3dCi 190 4WD

35282

L200 DIESEL - Double Cab DI-D 178 Warrior 4WD

25079

AMAROK A32 DIESEL - D/Cab Pick Up Highline 2.0 BiTDI 180 BMT 4MTN Auto

18622

L200 LWB LB DIESEL - Double Cab DI-D Barbarian 4WD 176Bhp

19135

NAVARA DIESEL - Double Cab Pick Up Tekna 2.5dCi 190 4WD

18623

L200 LWB LB DIESEL - Double Cab DI-D Barbarian 4WD Auto 176Bhp

With sales volumes returning to around the same levels we saw prior to the Christmas holiday slow down and a price performance of 101.2% it was another strong month for 4x4 Lifestyle Pick-ups according to our research data. On average the guide values have gone down by -0.3% or -£35 at 3 year/60K in this edition, however, there are number of exceptions which have had positive adjustments to the guide prices or are unchanged from last month. [*] We have also reviewed the price differentials between individual models in the MITSUBISHI L200 (15- ) DI-D LIFE model range in order to more accurately reflect current market sentiment.

|

Models |

|

|

ISUZU D-MAX DIESEL (17- ) (1%) |

TOYOTA HILUX (10-16) D-4D LIFE (0%) |

|

M-B X-CLASS DIESEL (2017- ) (4%) |

VW AMAROK (11-17) LIFE (1%) |

|

MITSUBISHI L200 (15- ) DI-D LIFE (0%)[*] |

FORD RANGER (11-16) PICK-UP LIFE (1%) |

|

NISSAN NAVARA E6 (16- ) LIFE (1%) |

ISUZU RODEO (03-07) LIFE (1%) |

|

VW AMAROK (16- ) LIFE (0%) |

MITSUBISHI L200 (01-07) TD/TD 113 LIFE (4%) |

|

ISUZU D-MAX DIESEL (12-18) (1%) |

NISSAN NAVARA (10-16) LIFE (1%) |

|

ISUZU RODEO (07-12) LIFE (1%) |

NISSAN NAVARA (05-07) LIFE (1%) |

|

MITSUBISHI L200 (06-16) DI-D LIFE (1%) |

4x4 Pick-ups Workhorse

CAPId

4x4 Pick-up Workhorse

30784

HILUX DIESEL - Active D/Cab Pick Up 2.5 D-4D 4WD 144

30783

HILUX DIESEL - Active Extra Cab Pick Up 2.5 D-4D 4WD 144

22413

RANGER DIESEL - Pick Up Double Cab XL 2.2 TDCi 150 4WD

26500

NAVARA DIESEL - Double Cab Pick Up Visia 2.5dCi 144 4WD

24963

D-MAX DIESEL - 2.5TD Double Cab 4x4

34428

DISCOVERY DIESEL - SE Commercial Sd V6 Auto

38351

HILUX DIESEL - Active D/Cab Pick Up 2.4 D-4D

16756

HILUX DIESEL - HL2 2010 D/Cab Pick Up 2.5 D-4D 4WD 144

18664

L200 LWB DIESEL - Pick Up DI-D 4Work 4WD 134Bhp [2010]

24962

D-MAX DIESEL - 2.5TD Extended Cab 4x4

With a 2.2% share of the total LCV sales in our research data and an average price performance of 101%, market prices held firm for most models in 4x4 Pick-up Workhorse sector. Toyota Hilux took 4 out of the Top 10 slots on sales volume and accounted for around 39% of all sector sales. Market prices at 3 year/60K fell by around 0.2% or -£14 in this sector, however, there are many exceptions listed below which have had positive guide price adjustments in this edition.

|

Models |

|

|

LAND ROVER (11-16) DEFENDER 90 110 130 TDCi (1%) |

MITSUBISHI SHOGUN (00-06) PET (4%) |

|

MITSUBISHI L200 (15- ) DI-D WORK (2%) |

NISSAN 1 TON (98-07) PICK-UP (1%) |

|

MITSUBISHI SHOGUN (14-18) (4%) |

NISSAN NAVARA (13-16) PICK UP (1%) |

|

NISSAN NAVARA E6 (16- ) PICK-UP (1%) |

NISSAN NP300 (08-10) PICK-UP (1%) |

|

MITSUBISHI L200 (10-16) DI-D WORK (2%) |

NISSAN TERRANO II (98-07) (1%) |

|

MITSUBISHI SHOGUN (00-16) (4%) |

MITSUBISHI L200 (04-07) TD/TD 113 WORK (2%) |

|

NISSAN NP300 NAVARA (16-16) PICK-UP (1%) |

NISSAN NAVARA (05-08) WORK (1%) |

|

NISSAN PATHFINDER (05-12) DIESEL (1%) |

NISSAN NAVARA (02-05) WORK (1%) |

|

MITSUBISHI L200 (06-10) DI-D WORK (2%) |

Ken Brown

LCV Valuations Editor

HGV MARKET OVERVIEW

With auctions getting back into full swing following the festive season it is refreshing to see some of them well attended and in some cases brisk business being done. It is still early days, but at the beginning of January the auctions which we attended initially indicated that values were down but by the end of the month the opposite was occurring and values across most sectors were showing signs of improvement back to the levels published last month.

One exception to the above was a major auction which had just two buyers in attendance, but good online interest saw it convert around 20% of the entries into hammer sales. January is always a strange month and often auctions see wildly differing action and values, usually it settles into a routine come February.

Stock appears to be increasing, as is usually the case at this time of year, and already one auction is using the car park as an overflow storage facility, which is all well and good but it creates havoc on sales days as customers struggle to find somewhere to park.

Traders report that it’s too early in the year to expect being busy and many are waiting for the end of winter before they expect business to pick up, despite the fact that the weather has been kind so far. That said, there are others who seem happy enough to buy for stock and are taking advantage of the post-Christmas stock currently available and the opportunity to secure a bargain.

One trader took the view that generally the quality of some of the older stock is too expensive for export and is not of suitable quality for the domestic market, rendering them unbuyable.

Manufacturers report continued healthy sales, one confirming breaking their own sales targets for the used vehicles. Continued low stocks of Euro 6 rigids helps their sale when they become available and it is comforting to see that despite the large stocks of tractor units some manufacturers have returning to them, trade is still being done.

It remains the case that except for tractor units there are few youthful Euro 6 vehicles finding their way into the auctions and when they do interest remains strong, providing that the kilometres are reasonable. High mileage examples are finding the going a little tough.

In 2019 registrations for HGV’s of 16 tonnes and over rose by 9.2% in the UK, with a total of 42,838 vehicles being registered, compared to 39,225 in 2018. The overall increase for the EU, (including the UK), was just 0.1% with a total of 312,692 vehicles registered against 312,483 in 2018. The increase in registrations will wash through to the used market in around five years’ time adding more vehicles to the current high volumes.

Records from our auction visits indicate that the average number of auction entries decreased by around 2.5% but the number of on-the-day truck increased by almost 17% in relation to total entries whilst trailer sales increased by 26% during the same period. This is based on three auction visits and a total of 479 viewed lots and as we always remind you these are ‘hammer sales’ on-the-day and converted provisional sales are not included. One auction has advised that the current conversion rates of provisional sales is around 50%, which is down 10% from last month, but hammer sales have increased.

As previously noted this month’s research suggests that values being both offered and achieved at auctions have been mixed during the month, starting low and generally improving as the month progressed and the market clearly hasn’t fully settled yet after Christmas.

7.5t to 12t Vehicles

Generally, in this range of vehicles those that have sold have seen values fluctuate recently, especially Euro 5 examples.

A large number of 2013 MAN TGL 7.5 tonne boxes from DX Freight and 2013 12 tonne DAF boxes from a leading truck rental company appeared on the auction circuit and whilst most are tidy enough to provoke interest, mileage plays a big factor in the prices being paid.

In the early part of the month higher mileage vehicles were realising bids substantially less than expected, but as the month progressed bids reflecting age and mileage had recovered. We will continue to monitor the situation before making any knee jerk changes to values.

Curtains and dropsides are less numerous than boxes and interest is slightly higher in these at present on a like for like basis. Tippers are suddenly far less numerous than in previous months, but fridges remain plentiful and most are well beyond their best.

Very little late Euro 6 stock has been seen, but those that do appear attract good interest especially if they have low mileage.

7.5t car transporters continue to provoke strong bidding whether they are tilt and slide or double decks. However, strong interest does not necessarily result in a sale and many operators seem to be favouring 12 tonne examples. Of which there has been a fair selection to choose from, including some 2014 crew cab Renault D12.240 tilt and slides and even with over 560,000 kilometres one sold for £35,000.

13t to 18t Vehicles

More 18 tonne fridges have become available as large batches have appeared, including a good number of Scania P230’s from the Co-Op. With plenty of DAF and Mercedes-Benz variants already available only the best ones are finding success.

More skip loaders have also become available and here too the best are being picked over, that said a couple of 14 plate MAN TGM 18.250’s struggled to muster mush interest.

Tidy 18t boxes and curtains are selling, especially those with sleeper cabs, but anything substandard and requiring reparation prior to use or re-sale often obtain little more than a nominal bid and are generally being shunned.

A selection of well-presented sweepers direct from a council operation stimulated good interest, including a 2015 DAF LF220 Johnston which sold for £63,000. A couple of very tidy twelve-year-old Mercedes-Benz Axor 1824 4x2 gritter/ploughs with very low mileage also proved popular lots and both sold on the day, doubtless their condition helping them on their way to new owners.

Multi-wheelers

As always it is tippers and crane vehicles that continue to shine although sales of both have slowed of late, no doubt an effect of the season.

A good selection of specialist vehicles from utility companies proved popular lots but whilst most had low mileages, their specialist nature can often work against them as operational opportunities remain low. Some did sell, once again aided by their condition and low mileage, but most remain to fight another sale.

Complete drawbar outfits continue to attract little interest. Several differing types of combinations have appeared recently and whilst most have been car carriers there have been boxes and brick and block carriers all of which failed to obtain bids enough to conclude a sale.

The availability of refuse trucks has increased significantly recently, and most continue to fail to attract realistic bids.

Tractor Units

The availability of Euro 6 6x2 examples continues to increase and we will continue to monitor the situation to see what if any affect it has on values as it is currently too early in the year to assess if there needs to be any movement in values, especially when prices fluctuated so much last month.

A substantial number of 4x2 units have recently appeared. A good selection of tidy 2011 Scania P360 sleepers from the Co-Op proved very popular and all sold on the day, and the values achieved appeared to suggest that 4x2 values are becoming more aligned with 6x2’s, helped in part by their relative scarcity. Another batch of 2013 Streamspace Mercedes-Benz 1842 didn’t fare so well, selling only in penny numbers, which could also suggest there is currently a ready export market for the Scania’s.

A small batch of Euro 6 Iveco Eurocargo ML75E19 7.5 tonne tractor units proved to be very popular lots, the best being a 2016 66 plate with 52,000 kilometres which sold for £18,750

Trailers

There has been little change in the market as the trailer sector continues to be steady and so far there has not been an influx of fresh trailers which often occurs post-Christmas

Most of the available trailers remain over ten years of age, often well over, so what little stock of newer trailers there is provokes good interest and often results in a sale.

Good quality tri-axle curtains, along with flats, have performed well recently, however one example, an as new 2014 flat, which was ready for immediate work proved a popular lot but it failed to meet its reserve value..

Tippers and low-loaders continue to attract attention and often, but not always sell, as and when they appear especially if they can be put straight to work.

Of interest at a recent sale was a new, unused, Rojo 4 axle machine carrier with SAF axles, drum brakes, hydraulic ramps, front lift axle and rear steer axle which achieved an offer of £42,000 but it failed to sell on the day.

Rob Smith

HGV Valuations Editor